One of the most affordable government-backed life insurance schemes in India is the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY). This scheme provides life insurance coverage at a very low annual premium, helping families stay financially protected in case the earning member passes away.

In a country where many households depend on a single source of income, the sudden loss of a family member can create serious financial difficulties. PMJJBY aims to reduce this risk by offering simple, affordable, and easily accessible life insurance, especially for low- and middle-income families.

This article explains PMJJBY in detail, including its features, eligibility, benefits, enrollment process, claim procedure, and why it is an important scheme for millions of Indians.

What is Pradhan Mantri Jeevan Jyoti Bima Yojana?

PMJJBY is a one-year renewable term life insurance scheme supported by the Government of India. It provides financial assistance of ₹2 lakh to the nominee in case of the subscriber’s death, regardless of whether the cause is natural or accidental.

The scheme is linked to the subscriber’s savings bank account, and the premium is paid through an auto-debit facility. It is offered by banks in partnership with life insurance companies.

The main objective of PMJJBY is to ensure that even individuals with limited financial resources can access basic life insurance protection.

Key Features of PMJJBY

The major highlights of the scheme include:

- Life insurance coverage of ₹2,00,000

- Annual premium of ₹436

- Coverage for death due to any cause

- Renewable every year

- Auto-debit facility from savings bank account

- Simple enrollment process with minimal paperwork

PMJJBY is purely a protection plan. It does not include any investment component or maturity benefit.

Why PMJJBY Was Introduced

A large number of people in India do not have life insurance coverage. Private insurance policies can be expensive and often require extensive documentation, medical tests, and higher premiums.

To address this gap, the government launched PMJJBY with the aim to:

- Make life insurance affordable and accessible

- Reduce financial vulnerability of families

- Promote financial inclusion

- Strengthen social security coverage

The scheme forms part of the government’s broader initiative to expand financial security among citizens.

Eligibility Criteria

To enroll in PMJJBY, a person must:

- Be between 18 and 50 years of age

- Have an active savings bank account

- Provide consent for auto-debit of the premium

If a person enrolls before turning 50, they can continue coverage up to the age of 55 by renewing annually and paying the premium on time.

Premium and Payment Details

The annual premium for PMJJBY is ₹436.

This amount is automatically deducted from the subscriber’s bank account, generally between May and June each year.

Benefits of Auto-Debit

- Ensures timely premium payment

- Prevents policy lapse

- Eliminates the need for manual renewal

- Provides convenience and reliability

Subscribers must ensure sufficient balance in their account during the premium deduction period to maintain uninterrupted coverage.

Coverage and Benefits

1. Life Insurance Coverage

Under PMJJBY, the nominee receives ₹2 lakh if the subscriber dies due to any reason—whether natural illness, accident, or other causes.

Unlike some insurance plans, there are no separate conditions for accidental death.

2. Financial Assistance to Family

The insurance payout can help cover:

- Daily household expenses

- Outstanding loans

- Children’s education

- Immediate emergency needs

Although ₹2 lakh may not fully replace the income of the deceased, it provides critical financial support during a difficult time.

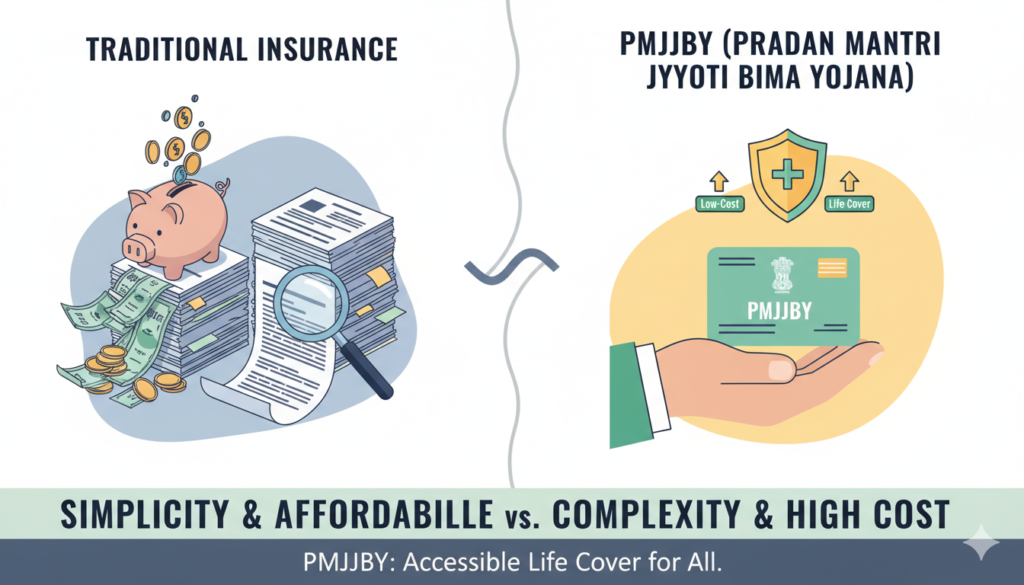

How PMJJBY Differs from Traditional Insurance Plans

PMJJBY differs from regular life insurance policies in several ways:

- No maturity benefit (no payout if the policyholder survives)

- Very low annual premium

- No investment or savings component

- Simplified enrollment process

- Basic protection-focused coverage

The scheme is designed primarily for risk coverage rather than wealth creation.

Who Should Enroll in PMJJBY?

PMJJBY is particularly suitable for:

- Daily wage earners

- Farmers

- Small shopkeepers

- Self-employed individuals

- Drivers and laborers

- Individuals without existing life insurance

If you are the primary earning member of your family and do not have life insurance coverage, PMJJBY can offer essential financial protection.

When Does Coverage Begin?

Coverage starts from the date of successful enrollment and premium deduction.

The policy remains valid for one year and must be renewed annually. In some cases, if enrollment occurs after the standard period, a self-declaration of good health may be required.

Reasons for Policy Termination

Coverage may end under the following conditions:

- The subscriber reaches 55 years of age

- Premium is not paid due to insufficient balance

- The linked bank account is closed

- Multiple enrollments are detected

To maintain active coverage, subscribers must ensure timely premium payment.

Claim Process Under PMJJBY

The claim procedure is simple and designed to make the process smooth for the nominee.

Steps to File a Claim:

- Inform the bank branch where the subscriber was enrolled.

- Obtain and complete the claim form.

- Submit required documents, including:

- Death certificate

- Duly filled claim form

- Identity proof of nominee

- The bank verifies and forwards the claim to the insurance company.

- Upon approval, the claim amount is credited to the nominee’s bank account.

The process is generally quicker and more straightforward than traditional life insurance claims.

How to Apply for PMJJBY

There are multiple ways to enroll:

1. Through a Bank Branch

- Visit your bank branch.

- Request the PMJJBY enrollment form.

- Fill in personal and nominee details.

- Sign consent for auto-debit.

The bank processes the application.

2. Through Internet Banking

Many banks offer online enrollment:

- Log into your internet banking account.

- Navigate to the insurance or social security schemes section.

- Select PMJJBY.

- Confirm details and authorize auto-debit.

The process usually takes only a few minutes.

3. Through Mobile Banking

Some banks also allow subscription through their mobile apps under government schemes.

Difference Between PMJJBY and PMSBY

PMJJBY is often confused with Pradhan Mantri Suraksha Bima Yojana (PMSBY).

The main difference is:

- PMJJBY covers death due to any cause.

- PMSBY covers accidental death and disability only.

Many individuals choose to enroll in both schemes for broader financial coverage.

Advantages of PMJJBY

- Extremely affordable premium

- Government-backed security

- Easy enrollment process

- Minimal documentation

- Financial support for dependents

- Accessible through banks across India

Its simplicity makes it suitable for both rural and urban populations.

Limitations of PMJJBY

Despite its benefits, the scheme has certain limitations:

- No maturity benefit

- Coverage limited to ₹2 lakh

- Age restrictions apply

- Requires annual renewal

Even with these limitations, PMJJBY remains one of the most accessible life insurance options available in India.

Important Points to Remember

- Keep nominee details updated.

- Inform your family about your enrollment.

- Maintain sufficient bank balance during premium deduction.

- Avoid multiple enrollments.

- Check renewal status annually.

Why PMJJBY is Important for India

A large segment of India’s workforce lacks formal social security coverage. Many families rely entirely on one earning member.

In such cases, the unexpected death of that individual can lead to severe financial distress. PMJJBY reduces this vulnerability by offering affordable life insurance coverage.

The scheme plays a significant role in strengthening financial stability among economically weaker sections and promoting inclusive growth.

Frequently Asked Questions

1. Is a medical examination required?

No medical test is required at the time of enrollment. However, a self-declaration of good health may be necessary in some cases.

2. Can I enroll through multiple bank accounts?

No. Multiple enrollments are not allowed and may result in termination.

3. Is the premium fixed?

The premium is currently ₹436 per year, but it may be revised by the government if required.

4. Can a lapsed policy be reinstated?

Yes, in certain cases, subject to specific conditions and payment of the premium.

Read: