The Atal Pension Yojana (APY) is a pension scheme backed by the Government of India that guarantees a fixed monthly income after the age of 60. It is specially designed for workers in the unorganized sector who do not receive formal retirement benefits such as EPF or corporate pensions.

The scheme was introduced to reduce financial insecurity in old age and to encourage individuals to build retirement savings during their working years. If you are between 18 and 40 years old and are not an income tax payer, APY can serve as a reliable financial support system for your future.

Objective of Atal Pension Yojana

The main goals of APY are:

- To provide subscribers with a guaranteed minimum pension.

- To protect individuals from longevity risk (the risk of outliving their savings).

- To promote a culture of retirement savings among workers in the unorganized sector.

- To offer a government-regulated and structured pension system.

The scheme is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) and operates under India’s pension reform framework.

Who Can Benefit?

APY is primarily intended for:

- Workers in the unorganized sector

- Daily wage earners

- Small shopkeepers and traders

- Self-employed individuals

- Domestic workers

- Farmers

- Drivers

- Construction workers

It is especially beneficial for economically weaker and underprivileged sections who generally lack access to formal pension arrangements.

Eligibility Criteria

To enroll in APY, the following conditions must be met:

- Age must be between 18 and 40 years.

- The applicant must have an active savings bank account.

- The applicant must not be an income tax payer (as per rules effective from 1 October 2022).

Pension Start Age

- Pension payments begin at 60 years of age.

- Contributions must continue regularly until the subscriber turns 60.

Contribution Structure

Contributions are automatically deducted from the subscriber’s savings bank account through an auto-debit facility.

Subscribers can choose to contribute:

- Monthly

- Quarterly

- Half-yearly

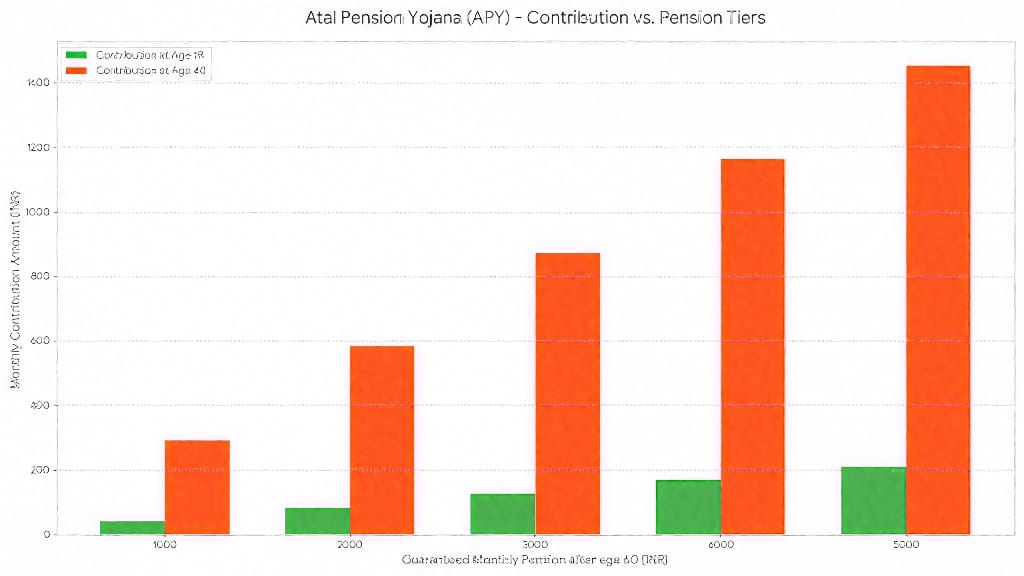

The contribution amount depends on:

- The age at which you join the scheme

- The pension amount selected (₹1000 to ₹5000 per month)

For example, if someone joins at 25 years of age and selects a ₹5000 monthly pension, their contribution will be lower than someone who joins at 35 for the same pension. Joining early reduces the contribution burden.

Guaranteed Pension Benefits

When the subscriber reaches 60 years of age, the following benefits are provided:

1. Guaranteed Monthly Pension

The subscriber will receive a fixed monthly pension of:

- ₹1000

- ₹2000

- ₹3000

- ₹4000

- ₹5000

The pension amount depends on the contribution plan chosen at the time of enrollment.

2. Pension for the Spouse

After the subscriber’s death, the spouse will continue to receive the same pension amount for the rest of their lifetime.

3. Return of Corpus to Nominee

After the death of both the subscriber and the spouse, the accumulated pension corpus will be paid to the nominee.

This structure ensures financial protection not only for the subscriber but also for the family.

Tax Benefits

Contributions made under APY qualify for tax benefits under Section 80CCD(1) of the Income Tax Act. The tax treatment is similar to that of the National Pension System (NPS).

Therefore, APY offers the dual advantage of retirement security and tax savings.

Charges, Fees, and Overdue Interest

Regular contributions are essential under the scheme. If there is:

- Delay in payment, or

- Non-payment of contribution

Then overdue interest and maintenance charges may be applied.

These charges are determined by PFRDA in consultation with the Central Government and may be revised from time to time. Maintaining regular payments helps avoid penalties and ensures uninterrupted benefits.

Voluntary Exit Before 60 Years

If a subscriber decides to exit the scheme before reaching 60 years:

- The individual will receive their own contributions along with the net actual income earned on them.

- Account maintenance charges will be deducted.

Important Note

Subscribers who joined before 31 March 2016 and received Government Co-Contribution will not receive that government contribution or the income earned on it in case of early exit.

Since APY is a long-term retirement scheme, early withdrawal is generally discouraged.

In Case of Death Before 60 Years

If the subscriber passes away before turning 60, two options are available:

Option 1: Spouse Continues the Scheme

- The spouse can continue contributing to the APY account.

- The account can be maintained in the spouse’s name.

- Pension will start when the original subscriber would have turned 60.

- The spouse will receive the same pension amount.

- This is allowed even if the spouse already has their own APY account.

Option 2: Return of Accumulated Corpus

- The total accumulated pension corpus up to that date will be paid to the spouse or nominee.

This flexibility ensures that the family remains financially secure.

Grievance Redressal

Subscribers can raise complaints at any time without any charges.

Steps to register a grievance:

- Visit www.npscra.nsdl.co.in

- Select “NPS-Lite”

- Use the CGMS portal

- Register your grievance

A token number will be generated after submission, which can be used to track the complaint status online.

How to Apply for APY

APY can be opened both online and offline.

Online Through Net Banking

- Log in to your internet banking account.

- Search for “Atal Pension Yojana.”

- Fill in personal and nominee details.

- Provide consent for auto-debit.

- Submit the application.

Registration is completed digitally.

Online Through eNPS Portal

- Visit the official eNPS website.

- Select “Atal Pension Yojana.”

- Click on “APY Registration.”

- Complete KYC through one of the following methods:

- Offline Aadhaar XML upload

- Aadhaar OTP verification

- Virtual ID-based KYC

- Fill personal details.

- Select pension amount and contribution frequency.

- Provide nominee details.

- Complete eSign verification.

You can also enroll through the e-APY portal or participating bank websites.

Offline Application

- Visit your bank branch or post office.

- Request the APY form.

- Fill in required details and nominee information.

- Sign the auto-debit authorization.

- Submit the form to complete registration.

Documents Required

No extensive documentation is required. KYC details are typically retrieved from:

- Active Savings Bank Account

- Post Office Savings Account

If Aadhaar is linked to your account, the process becomes quicker and simpler.

Helpline Number

Toll-free helpline for APY:

1800-110-069

You can call for assistance regarding:

- Registration

- Contribution details

- Pension calculations

- Complaint support

Why APY Matters

A large portion of India’s workforce is employed in the unorganized sector. Many workers:

- Do not receive EPF benefits.

- Do not have employer-sponsored pension plans.

- Depend on savings or family support in old age.

APY addresses this gap by offering:

- Guaranteed pension income

- Financial protection for spouse

- Nominee benefits

- A disciplined savings structure

It promotes financial independence and dignity in retirement.

Key Advantages of APY

- Government-backed guarantee

- Affordable contribution amounts

- Flexible payment frequency

- Auto-debit convenience

- Tax benefits

- Family security

- Low administrative cost

Important Points to Remember

- Enroll early to reduce contribution amounts.

- Maintain sufficient balance in your bank account.

- Keep nominee details updated.

- Inform the bank about any changes in contact details.

- Avoid missed payments to prevent penalties.

Frequently Asked Questions

1. Can I change my pension amount later?

Yes, subscribers can modify their pension amount once every year.

2. Is APY safe?

Yes, the scheme is regulated by PFRDA and supported by the Government of India.

3. Can NRIs join APY?

Only eligible Indian citizens can enroll.

4. What happens if I miss contributions?

Penalties may apply, and prolonged non-payment could lead to account closure.

Conclusion

The Atal Pension Yojana is one of the most affordable and accessible pension schemes available in India. It ensures a guaranteed income after retirement while also providing financial protection for the spouse and nominee.

For workers in the unorganized sector, APY offers a practical and disciplined way to build long-term financial security. Starting early allows you to contribute smaller amounts and maximize the benefits.

Retirement planning is essential, not optional. The Atal Pension Yojana makes it structured, affordable, and dependable.